Polski

Polski

STANDBY LETTER OF CREDIT (SBLC)

A legal instrument issued by a bank on behalf of its client, providing a guarantee of its commitment

to pay the seller if its client (the buyer) defaults on the agreement

What is a Standby Letter of Credit (SBLC)?

A standby letter of credit, abbreviated as SBLC, refers to a legal document where a bank guarantees the payment of a specific amount of money to a seller if the buyer defaults on the agreement.

An SBLC acts as a safety net for the payment of a shipment of physical goods or completed service to the seller, in the event something unforeseen prevents the buyer from making the scheduled payments to the seller. In such a case, the SBLC ensures the required payments are made to the seller after fulfillment of the required obligations.

A standby letter of credit is used in international or domestic transactions where the seller and the buyer do not know each other, and it attempts to hedge out the risks associated with such a transaction. Some of the risks include bankruptcy and insufficient cash flows on the part of the buyer, which prevents them from making payments to the seller on time.

In case of an adverse event, the bank promises to make the required payment to the seller as long as they meet the requirements of the SBLC. The bank payment to the seller is a form of credit, and the customer (buyer) is responsible for paying the principal plus interest as agreed with the bank.

Summary

- A standby letter of credit (SBLC) refers to a legal instrument issued by a bank on behalf of its client, providing a guarantee of its commitment to pay the seller if its client (the buyer) defaults on the agreement.

- An SBLC is used in international and domestic transactions where the parties to a contract do not know each other.

- A standby letter of credit serves as a safety net by assuring the seller that the bank will make payment for the goods or services delivered if the buyer fails to make the payment on time.

Standby Letter of Credit Explained

A standby letter of credit is often required in international trade to help a business obtain a contract. Since the parties to the contract do not know each other, the letter promotes the seller’s confidence in the transaction. It is seen as a sign of good faith since it shows the buyer’s credit quality. Creditworthiness, simply put, is how “worthy” or deserving one is of credit. If a lender is confident that the borrower will honor her debt obligation in a timely fashion, the borrower is deemed creditworthy, and ability to make payment for goods or services even if an unforeseen event occurs.

When setting up an SBLC, the buyer’s bank performs an underwriting duty to verify the credit quality of the buyer. Once the buyer’s bank is satisfied that the buyer is in good credit standing, the bank sends a notification to the seller’s bank, assuring its commitment of payment to the seller if the buyer defaults on the agreement. It provides proof of the buyer’s ability to make payment to the seller.

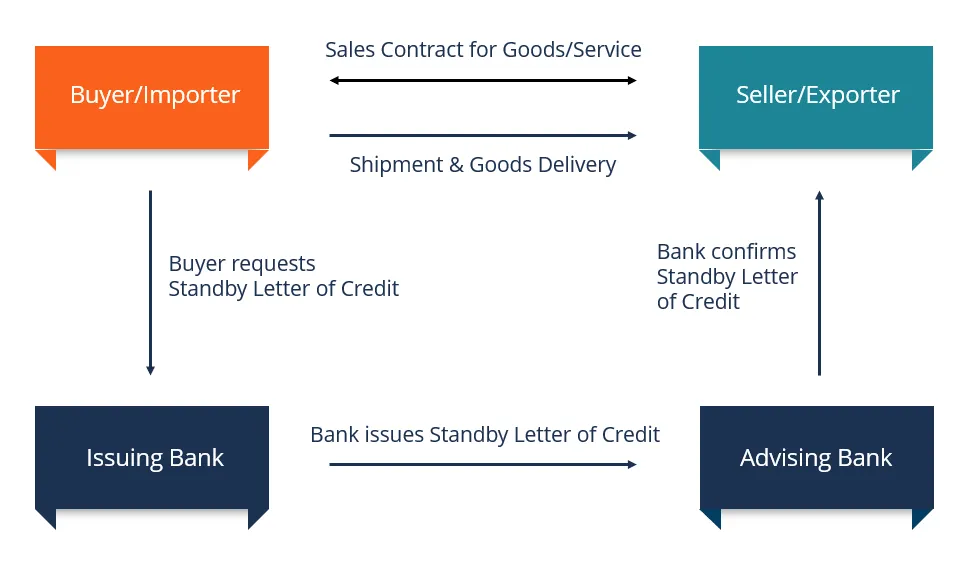

How an SBLC Works

The process of obtaining an SBLC is similar to a loan application process. The process starts when the buyer applies for an SBLC at a commercial bank. The bank will perform its due diligence on the buyer to assess its creditworthiness, based on past credit history and the most recent credit report. If the buyer’s creditworthiness is in question, the bank may require the buyer to provide an asset or the funds on deposit as collateral before approval.

The level of collateral will depend on the risk involved, the strength of the business, and the amount secured by the SBLC. The buyer will also be required to furnish the bank with information about the seller, shipping documents required for payment, the beneficiary’s bank, and the period when the SBLC is valid.

After review of the documentation, the commercial bank will provide an SBLC to the buyer. The bank will charge a service fee of 1% to 10% for each year when the financial instrument remains valid. If the buyer meets its obligations in the contract before the due date, the bank will terminate the SBLC without a further charge to the buyer.

If the buyer fails to meet the terms of the contract due to various reasons, such as bankruptcy, cash flow crunch, dishonesty, etc., the seller is required to present all the required documentation listed in the SBLC to the buyer’s bank within a specified period, and the bank will make the payment due to the seller’s bank.

Types of Standby Letter of Credit

The two main types of SBLC are:

1. Financial SBLC

The financial-based SBLC guarantees payment for goods or services, as stipulated in the agreement. For example, if a crude oil ships oil to a foreign buyer with an expectation that the buyer will pay within 30 days from the date of shipment, and the payment is not made by the required date, the crude oil seller can collect the payment for goods delivered from the buyer’s bank. Since it is a credit, the bank will collect the principal plus interest from the buyer.

2. Performance SBLC

A performance-based SBLC guarantees the completion of a project within the scheduled timelines. If the bank’s client is unable to complete the project outlined in the contract, then the bank promises to reimburse the third party to the contract a specific sum of money.

Performance SBLCs are used in projects that are scheduled for completion within a specific timeline, such as construction projects. The payment serves as a penalty for delays in the project’s completion, and it is used to compensate the customer for the inconvenience caused or pay another contractor to take over the project.

Top